The economic impact of climate change is becoming increasingly alarming as new research suggests that the financial toll could be far greater than previously estimated. Recent climate change economic projections indicate that each incremental increase in global temperatures could unleash a 12 percent decline in global GDP, shedding light on the profound effects of rising temperatures. With extreme weather events becoming more common and destructive, understanding the cost of climate change has never been more essential for policymakers and economists alike. In light of recent studies, decarbonization policies are now recognized not just as environmentally necessary but also as economically beneficial, with projections showing that failing to act could lead to financial devastation similar to the Great Depression. As we navigate these challenges, it is crucial to consider the long-term implications of climate change on our economy and the steps needed to mitigate its impacts.

The financial ramifications of climate change, often referred to as the ecological economy, are capturing the attention of scientists and economists worldwide. New assessments illustrate the substantial economic repercussions that rising temperatures can have on global productivity, inevitably reshaping economic landscapes. The urgency to address climate shifts is matched by the growing calls for robust policies aimed at decarbonization, as studies reveal that the costs associated with inaction—ranging from decreased consumption to increased disaster recovery expenses—are monumental. As extreme weather patterns escalate, the need for thorough economic evaluations—encompassing everything from GDP fluctuations to investment in sustainable practices—becomes increasingly critical. These insights reflect an emerging paradigm where sustainability and economic stability are intertwined, prompting a re-evaluation of our current trajectory in addressing climate challenges.

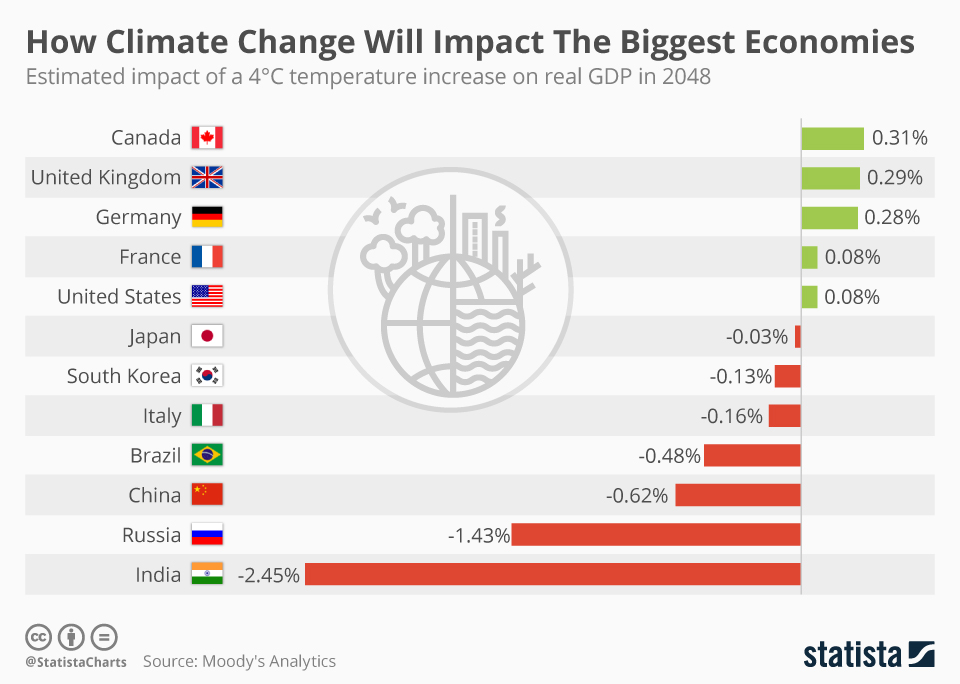

Understanding the Economic Impact of Climate Change

The economic impact of climate change is a pressing concern that has gained increasing attention in recent years. In a notable study by economists Adrien Bilal and Diego R. Känzig, new projections suggest that for every additional degree Celsius increase in global temperatures, we could witness a staggering 12 percent decline in global GDP. This marks a substantial shift from earlier estimates, which painted a less alarming picture of economic losses associated with climate change. The economic ramifications of rising temperatures extend beyond mere monetary values; they encompass widespread effects on productivity, spending, and overall economic stability.

Moreover, the ramifications are not limited to long-term forecasts; they are immediate and escalating. For instance, extreme weather events such as hurricanes, heatwaves, and floods are becoming increasingly common, leading to direct economic disruption. The interconnectedness of global economies means that the consequences of climate change in one region can ripple across the globe. As such, understanding the economic impact of climate change is critical for policymakers formulating effective responses that can mitigate these risks and promote resilience in affected communities.

Climate Change Economic Projections and Their Implications

Recent economic projections related to climate change indicate a dire forecast for the global economy. Bilal and Känzig’s research reveals that a 2°C rise by the end of the century could lead to a 50 percent decline in output and consumption, an economic downturn that would dwarf the Great Depression in scale and duration. Such projections underscore the urgent need for robust policy interventions and decarbonization strategies that prioritize long-term sustainability over short-term gains. The economic cost of inaction is immense, raising crucial questions about how we can reconcile growth with ecological responsibility.

In light of these projections, it becomes evident that current approaches to climate change economic modeling may be overly simplistic. Traditional metrics often fail to capture the complex interplay between economic growth, climate factors, and extreme weather occurrences. The shift towards integrating global temperature as a primary variable in economic forecasts represents a significant advancement in our understanding of climate-related risks. It enables policymakers to develop more informed decarbonization policies that not only focus on mitigation but also on fostering economic resilience against future climate impacts.

The Cost of Climate Change: A New Perspective

Revising the cost of climate change from an economic standpoint requires a fresh perspective on how we value environmental impacts. The recent examination by Bilal and Känzig articulates a social cost of carbon that closely aligns with modern climate data, estimating it at $1,056 per ton. This figure is significantly higher than previous estimations, emphasizing that the pressing nature of climate change should invoke a serious reevaluation of current economic beliefs. Clearly, failing to account for the true costs associated with climate change can mislead policy decisions and investment strategies, ultimately exacerbating economic vulnerabilities.

Furthermore, the analysis highlights the importance of incorporating adaptation strategies along with mitigation efforts to address the burgeoning costs of climate change. As global temperatures continue to rise, the economic burden of inaction will only escalate, necessitating immediate and efficient responses. One promising avenue involves enacting decarbonization policies that not only mitigate emissions but also support investment in resilience-building initiatives. In doing so, economies can transition towards a sustainable growth path while lowering the long-term economic costs associated with climate change.

Extreme Weather and Economic Disruption

The rise in extreme weather events as a consequence of climate change poses significant economic challenges. As highlighted by the recent findings of Bilal and Känzig, the frequency and intensity of such events directly correlate with increases in global temperatures. From hurricanes that devastate infrastructure to heatwaves that reduce agricultural yields, the fallout from these disruptions translates to profound economic costs and productivity losses. Local economies, heavily reliant on stable weather patterns, find themselves increasingly vulnerable to the unpredictable nature of climate-related phenomena.

The repercussions of extreme weather extend far beyond immediate damages, affecting long-term economic growth and resilience. Research indicates that regions that experience frequent extreme weather suffer from decreased investment and higher insurance costs, which further places them at a competitive disadvantage. To counteract these economic vulnerabilities, it’s essential for governments and businesses to adopt comprehensive risk management strategies that address both the immediate impacts of extreme weather as well as their long-term socioeconomic implications.

Decarbonization Policies and Economic Growth

The successful implementation of decarbonization policies is not just a necessary step to combat climate change; it can also serve as a catalyst for economic growth. Bilal and Känzig illustrate through their research that aggressive decarbonization initiatives can pass the cost-benefit analysis criteria, suggesting that investing in green technologies and renewable energy sources may yield significant economic dividends. By prioritizing these policies, economies can transition towards lower carbon footprints while capitalizing on the growing demand for sustainable solutions.

Investments in clean technology have the potential to create millions of jobs while fostering innovation across various sectors. As economies shift their focus towards decarbonization, there is an opportunity to align economic prosperity with environmental responsibility. The intersection of economic growth and sustainable practices provides a pathway not only to mitigate climate change but also to secure healthier, more resilient futures for upcoming generations.

Global GDP Decline: A Looming Threat

Amidst the alarming forecasts surrounding climate change, the projected decline in global GDP is one of the most significant and far-reaching concerns. The research conducted by Bilal and Känzig indicates that as global temperatures rise, we face a potential 12 percent reduction in GDP for every degree increase, projecting severe repercussions for worldwide economic stability. Such declines can exacerbate existing inequalities, disrupt international trade patterns, and challenge global supply chains that are already under strain from other crises.

Understanding the implications of a potential global GDP decline necessitates concerted action on multiple fronts. Policymakers must prioritize adaptive measures that not only promote economic stability but also safeguard vulnerable populations from economic shocks associated with climate change. By embedding climate considerations within economic planning and prioritizing investments in resilience, nations can better navigate the complexities of changing climates to sustain overall economic health.

Investing in Climate Resilience

Investing in climate resilience is paramount for minimizing the economic toll of climate change. The findings from Bilal and Känzig emphasize that proactive measures are essential to both mitigate climate risks and safeguard economic vitality. This entails enhancing infrastructure, investing in sustainable agricultural practices, and integrating climate risk assessments into financial decision-making. By prioritizing resilience-building initiatives, countries can create a buffer against potential disruptions caused by climate change, ensuring that they remain on a sustainable growth trajectory.

Moreover, investments in climate resilience not only protect assets but also stimulate local economies. Creating green jobs, facilitating training programs for emerging sectors, and fostering community engagement are all vital components of a resilient economy. As nations pivot towards a future that acknowledges the reality of climate change, such investments will prove integral not only for recovery but for long-term sustainability and socioeconomic well-being.

Policy Responses to Climate Change Economics

Effective policy responses to the economic challenges posed by climate change are crucial in navigating the intricacies of this global issue. The insights from Bilal and Känzig provide a compelling case for rethinking existing economic models and frameworks. Policymakers must adopt a comprehensive approach that prioritizes the integration of climate science into economic forecasting, ensuring that decision-making reflects the potential impacts of climate change on both local and global scales. This involves direct engagement with economic stakeholders and the incorporation of scientific data in policy design.

Furthermore, developing adaptive and forward-thinking policies will enhance resilience against the chronic risks posed by climate change. Establishing incentives for businesses to implement sustainable practices, supporting innovation in green technologies, and facilitating international collaboration to deal with shared climatic challenges are pivotal aspects of any effective response. By embracing a holistic framework that fosters cooperation and innovation, governments can position their economies to better withstand the shifts brought about by climate dynamics.

The Role of Technological Innovation in Addressing Climate Change

Technological innovation plays a critical role in addressing the economic impacts of climate change. As demonstrated by recent studies, advancements in clean energy technologies and increased efficiency in resource use can lead to significant reductions in greenhouse gas emissions. These innovations not only mitigate the immediate effects of climate change but also create new economic opportunities and jobs in emerging industries. The economic cost of inaction can be mitigated through a concerted focus on research and development that prioritizes sustainable solutions.

Moreover, the potential for technological advancements to transform sectors such as transportation, agriculture, and energy is immense. Transitioning to electric vehicles, implementing precision agriculture techniques, and enhancing renewable energy infrastructure can yield both environmental and economic benefits. By catalyzing innovation and ensuring that policies support the adoption of clean technologies, economies can pave the way for sustainable growth that reconciles developmental goals with climate resilience.

Frequently Asked Questions

What is the projected economic impact of climate change on global GDP?

Recent studies indicate that every 1°C rise in global temperatures could lead to a 12 percent decline in global gross domestic product (GDP). This projection suggests that the economic impact of climate change is significantly more severe than previously estimated, with potential losses peaking shortly after the temperature increase.

How do extreme weather events influence the economics of climate change?

Extreme weather events, which increase in frequency and severity with global temperature rises, can severely affect productivity and capital. As temperatures rise, countries may experience more heat waves, floods, and storms, all of which contribute to economic disruptions and losses in productivity, emphasizing the rising cost of climate change.

What are decarbonization policies and their role in mitigating climate change’s economic impact?

Decarbonization policies aim to reduce carbon emissions to combat climate change and its associated economic costs. Implementing such policies has been shown to yield benefits that surpass their costs, with recent analysis suggesting that large economies like the U.S. and EU can greatly benefit from these initiatives, particularly in light of the high social cost of carbon.

How does the cost of climate change compare to the social cost of carbon?

Recent research estimates the social cost of carbon at approximately $1,056 per ton globally. This figure starkly contrasts with older estimates of $185 per ton. Understanding this discrepancy is critical, as it highlights the increasing economic impact of climate change and underscores the economic viability of decarbonization policies.

What historical comparisons can be made about economic losses from climate change?

If global temperatures rise by an additional 2°C by 2100, the projected decline in output and consumption could be as severe as a 50 percent reduction. This potential loss is twice the economic downturn experienced during the Great Depression, underscoring the alarming long-term economic consequences of climate change.

| Key Points | Details |

|---|---|

| New Economic Projections | Study estimates economic toll of climate change six times larger than previous estimates. |

| Projected GDP Decline | Every additional 1°C rise in temperature predicted to cause a 12% decline in global GDP. |

| Impact of Temperature Variations | Research highlights the connection between global temperature rises and extreme weather occurrences influencing productivity. |

| Social Cost of Carbon | New estimate for global social cost of carbon is $1,056 per ton, significantly higher than previous estimates. |

| Potential Impact by 2100 | If global temperatures rise an additional 2°C, a 50% reduction in output and consumption is expected. |

Summary

The economic impact of climate change is becoming increasingly alarming, with new research suggesting that the potential financial losses could be far more severe than previously thought. A recent study indicates that every 1°C increase in global temperatures could result in a 12% decline in global GDP, highlighting a critical need for urgent policy discussions and decarbonization strategies. As we look towards the future, understanding the profound effects of climate change on economic productivity is essential for devising effective solutions that can mitigate these impacts.