The 2017 Tax Cuts and Jobs Act (TCJA) marked a significant shift in the landscape of U.S. tax policy, aiming to spur economic growth through lowered corporate tax rates. This controversial legislation not only reduced the corporate tax rate from 35% to 21% but also introduced a series of tax reform effects that have made waves in political discourse. Critics and supporters alike continue to debate the impact of the TCJA, particularly in relation to wage increases and business investments. Leading this analysis is Harvard economist Gabriel Chodorow-Reich, whose research scrutinizes the real outcomes of the corporate tax cuts. As Congress prepares for a tax battle in 2025, understanding the long-term implications of the TCJA has never been more crucial for voters and policymakers alike.

The Tax Cuts and Jobs Act of 2017, a pivotal piece of legislation, reshaped the American tax framework with its focus on slashing corporate tax rates. As ongoing discussions unfold about the implications of such tax changes, analysts like Gabriel Chodorow-Reich have emerged to provide a comprehensive tax policy analysis that highlights the varied outcomes of this reform. The discussions around this legislation are not merely about numbers but involve understanding the broader economic impacts, including potential wage increases for workers and the overall health of business investments. As the expiration of key provisions draws near, the debate over corporate taxation continues to intensify, revealing insights into the complex interplay between tax policy and economic growth. The effects of this landmark act remain a critical focal point in the upcoming legislative discussions, shaping the trajectory of American economic policy.

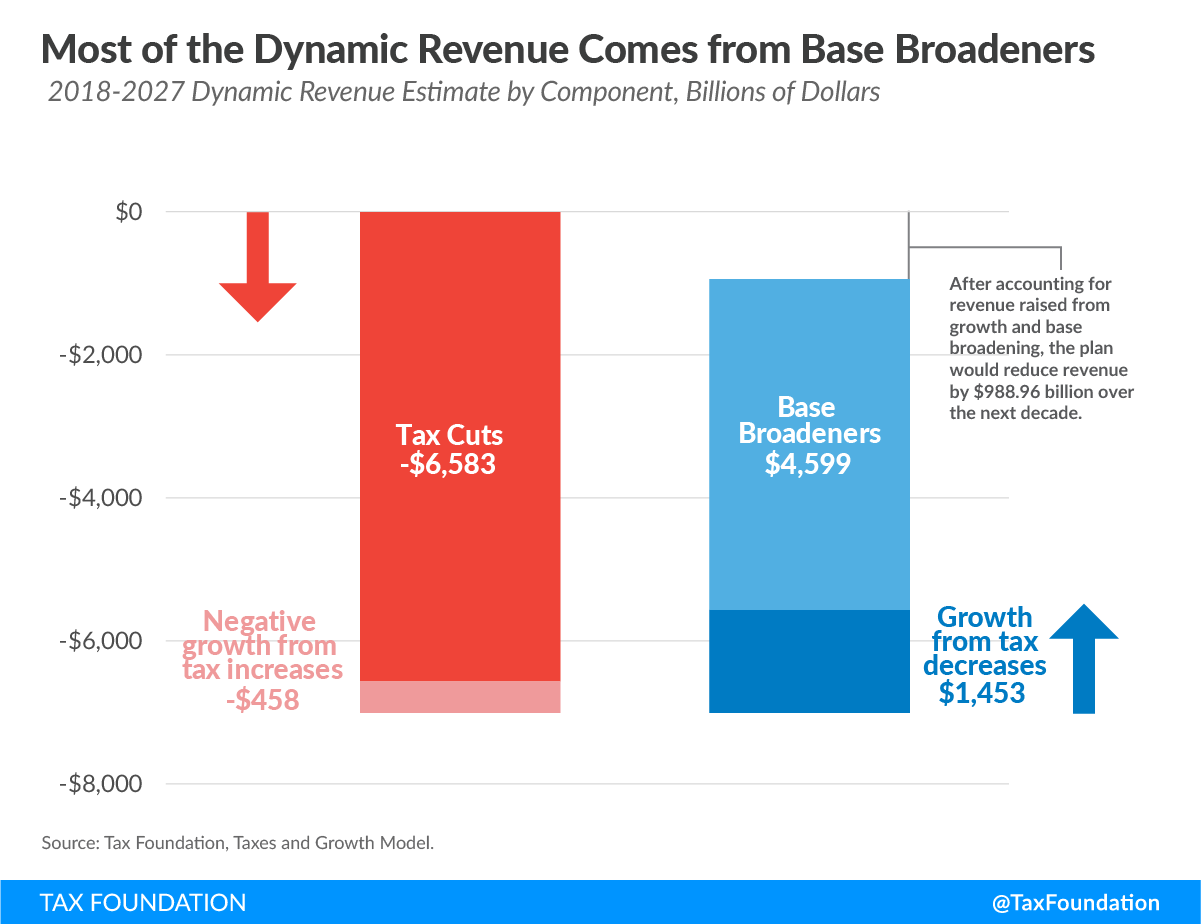

The Impact of the 2017 Tax Cuts and Jobs Act on Corporate Tax Rates

The 2017 Tax Cuts and Jobs Act (TCJA) marked a significant shift in U.S. tax policy by reducing the corporate tax rate from 35% to 21%. This reform aimed to make U.S. corporations more competitive globally, especially as other nations were slashing their rates. Economists like Gabriel Chodorow-Reich argue that while the TCJA has led to increased corporate investment, the actual benefits in terms of wage growth and tax revenue recovery have been modest. Analysis of corporate tax returns suggests that the immediate effects of this tax rate cut were not as transformative as anticipated, raising questions about the long-term sustainability of such a drastic change in tax policy.

Chodorow-Reich’s studies highlight the nuances in the aftermath of these cuts. While there was an observable uptick in capital investments—estimated at around 11%—the expected surge in employee wages did not mirror this optimistic outlook. Instead of the predicted annual wage increases of $4,000 to $9,000 per employee, actual figures hovered around $750. This disparity between expected and actual outcomes raises vital discussions about the effectiveness of tax reform and points toward a need for a balanced approach in future tax policy that considers both corporate needs and worker welfare.

Analyzing the Long-term Effects of Tax Reform on Wage Increases

The debate over the TCJA continues as many economists examine its long-term effects on wage increases for workers. Gabriel Chodorow-Reich and his colleagues emphasize that while corporate tax cuts can incentivize investment in business, their impact on wages is far less certain. The initial wave of tax reform was expected to yield significant benefits for employees through increased corporate spending on labor, but the results have not aligned with these predictions. As businesses sought to optimize their any potential gains from tax savings, many did not translate this into substantial wage increases for their employees.

One of the challenges in assessing the true impact of the TCJA on wages lies in the varying methods of analyzing economic data. While some reports indicate minimal wage growth, alternative evaluations suggest that strategic reinvestment in businesses could eventually lead to improved labor conditions. Advocates for tax reforms argue that restoring provisions that encourage more targeted investments—such as immediate expensing—could provide more direct benefits to workers. As the political landscape shifts with upcoming elections, detailed tax policy analysis will be essential to inform lawmakers and voters alike about the real repercussions of corporate tax decisions.

The Role of Corporate Tax Rates in Economic Growth

Corporate tax rates are often hailed as a key lever in stimulating economic growth, and the TCJA was designed to achieve just that. By slashing tax rates significantly, proponents argued that companies would have more capital to invest in innovation, infrastructure, and workforce development. However, as Gabriel Chodorow-Reich notes, the reality is more complicated. While there was a rise in business investments following the TCJA, the correlation between corporate tax cuts and improved economic indicators like wage increases remains tenuous at best.

Emerging research suggests that it’s not just the statutory corporate tax rate itself that influences business behavior and economic prosperity but rather how these tax policies interact with other economic factors and incentives. For example, temporary provisions aimed at expensing investments have shown to produce more immediate benefits than static tax cuts. This insight may encourage policymakers to consider a more nuanced approach going forward, one that couples corporate tax rate adjustments with targeted incentives that stimulate direct economic benefits for average workers.

Evaluating the Economic Claims Surrounding Tax Reform

Tax reform debates often hinge on varying projections about their potential impacts. The TCJA was marketed as a way to fuel U.S. economic growth and create jobs, yet the range of estimates on these claims has created friction among economists and policymakers. Gabriel Chodorow-Reich’s analysis in the Journal of Economic Perspectives aims to clarify these discussions by scrutinizing the data behind the economic claims surrounding tax cuts. His findings challenge the narrative that tax reductions automatically lead to increased investment and higher wages for the working class.

Critics of the TCJA argue that the immediate financial benefits touted as a result of lower corporate tax rates are not a straightforward reflection of reality. Many companies opted to boost shareholder value rather than reinvest in employee wages or job creation. Thus, while the tax cuts have undeniably impacted business investments, the larger dialogue about how these reforms affect broader economic health continues to evolve, necessitating continued analysis and discourse on responsible tax policy.

The Future of Corporate Tax Cuts in Legislative Discussions

As Congress approaches potential tax battles in 2025, the future of corporate tax cuts remains a contentious topic. Key provisions from the TCJA are set to expire, prompting renewed discussions among lawmakers. Figures like Vice President Kamala Harris advocate for raising corporate tax rates to fund progressive initiatives, while opponents, including former President Donald Trump, argue for further tax cuts as a means of promoting economic growth. This ideological division underscores the complex landscape in which economic policy is formulated regarding corporate taxation.

Discussions about the TCJA’s legacy are not merely about fiscal outcomes; they also reflect deeper ideological divides over how best to spur economic development. Chodorow-Reich’s research contributes to this dialogue by offering data-driven insights that can shape future legislative strategies. Policymakers must weigh the consequences of tax policy adjustments carefully, as they grapple with voter concerns surrounding taxation, economic growth, and the overarching goals of equity and sustainability in America’s economic landscape.

Corporate Tax Policy: Analyzing Evidence and Impact

The discourse on corporate tax policy is increasingly anchored in empirical evidence, as exemplified by Gabriel Chodorow-Reich’s recent study that evaluates the impact of the TCJA on corporate behavior. His work highlights the importance of analyzing tax data not just in terms of statutory rates but in observing how firms respond to various tax incentives. The results show that while corporate tax cuts led to increased investment, the parallel expectations of wage growth and enhanced job security remain a vital area for ongoing scrutiny.

Understanding how corporate tax policy influences the broader economy is crucial for making informed legislative decisions. As seen with the TCJA, tax reductions can inspire short-term business optimism but may not always translate to sustained economic benefits for the workforce. It is necessary for future tax policy analysis to emphasize adaptable strategies that incentivize genuine growth while ensuring that the accompanying benefits extend beyond the corporate level, reaching employees and households that underpin our economy.

Public Opinion and the 2017 Tax Cuts: Understanding Voter Concerns

Public opinion plays a significant role in shaping tax policy discussions, especially as provisions of the 2017 Tax Cuts and Jobs Act face expiration. While many citizens express concern regarding the potential increase in tax rates for corporations, a closer examination reveals that the electorate is equally apprehensive about how these tax policies affect their daily lives. Voter perspectives focus on tangible benefits, such as the Child Tax Credit, which directly impacts household financial stability.

As political parties gear up for debates leading into the next election cycle, the importance of addressing these voter concerns cannot be overstated. Economists like Gabriel Chodorow-Reich emphasize the need for comprehensive tax reform that reassures voters of equitable growth and addresses the disparity between corporate profits and individual wage growth. Balancing corporate interests with the needs of constituents will be crucial in developing a tax framework that garners public support and addresses the realities of economic inequality.

Implications of Corporate Tax Policy on Investment Strategies

Corporate tax policy directly influences investment strategies across sectors. The TCJA introduced several incentives meant to promote capital investment, such as allowing companies to expunge the costs related to new equipment immediately. Gabriel Chodorow-Reich’s research indicates that while certain provisions sparked an increase in capital investments, understanding the mechanisms that underpin these changes is essential for future policy development.

The implications of tax policy on investment decisions may offer pathways for refining corporate incentives. As lawmakers review past tax reforms, lessons learned from the TCJA can inform potential adjustments aimed at improving the functionality of corporate tax code. By fostering an investment climate that aligns with both corporate objectives and broader economic goals, legislators can craft tax policies that yield systemic benefits, ensuring a more robust economic future.

Strategizing for Future Tax Reforms: Lessons from Past Legislation

Looking ahead, the lessons learned from the 2017 Tax Cuts and Jobs Act will serve as critical guideposts for future tax reforms. Policymakers are tasked with navigating a complex landscape characterized by public demands for economic fairness and the need for stimulating growth. Gabriel Chodorow-Reich’s insights underscore the necessity for a strategic approach that blends tax rate considerations with targeted tax incentives that address investment while promoting equitable growth across income levels.

Future legislative efforts should prioritize comprehensive analyses that incorporate various socioeconomic variables, focusing on how corporate tax reforms can influence overall economic dynamics. By leveraging past experiences and current research, lawmakers can aspire to create a more balanced tax structure that meets both national prosperity goals and the aspirations of individual taxpayers, ensuring that reforms do not disproportionately favor corporate interests at the expense of working families.

Frequently Asked Questions

What are the key changes introduced by the 2017 Tax Cuts and Jobs Act regarding corporate tax rates?

The 2017 Tax Cuts and Jobs Act permanently reduced the corporate tax rate from 35% to 21%, aimed at fostering business growth and increasing global competitiveness.

How did the 2017 Tax Cuts and Jobs Act affect wage increases according to recent studies?

Studies, including those by economist Gabriel Chodorow-Reich, indicate that the 2017 Tax Cuts and Jobs Act resulted in modest wage increases, estimated at around $750 per year, which is significantly lower than the projected increases of $4,000 to $9,000 per employee.

What were the economic effects of the corporate tax cuts under the 2017 Tax Cuts and Jobs Act?

The corporate tax cuts under the 2017 Tax Cuts and Jobs Act initially led to a 40% drop in federal corporate tax revenue, but by 2020, revenues began to recover thanks to unexpected surges in business profits.

What impact did the 2017 Tax Cuts and Jobs Act have on business investments?

The 2017 Tax Cuts and Jobs Act spurred approximately an 11% increase in business investments, particularly through key provisions that allowed firms to expensively deduct the full cost of new capital investments.

How does Gabriel Chodorow-Reich’s analysis contribute to the discussion about tax reform effects of the 2017 Tax Cuts and Jobs Act?

Gabriel Chodorow-Reich’s analysis challenges common narratives by showing that while corporate tax cuts have some impact on investment, the revenue losses were significant and the wage increases were modest, prompting a reevaluation of tax policy analysis.

Are there any proposed changes to the corporate tax rates after the expiration of parts of the 2017 Tax Cuts and Jobs Act?

With key provisions of the 2017 Tax Cuts and Jobs Act set to expire, there have been discussions about potentially raising corporate tax rates to restore revenue and fund initiatives.

What are the future implications of the 2017 Tax Cuts and Jobs Act on tax policy?

As key provisions of the 2017 Tax Cuts and Jobs Act approach expiration, lawmakers will need to balance the desire for lower corporate tax rates with the need for adequate tax revenue to support government programs.

What role did international competition play in the 2017 Tax Cuts and Jobs Act?

International competition influenced the 2017 Tax Cuts and Jobs Act as the U.S. faced increasing pressure to lower corporate tax rates to remain competitive with other nations that had significantly reduced their tax burdens.

| Key Provisions | Impacts | Political Context | Revenue Effects |

|---|---|---|---|

| Reduced corporate tax rate from 35% to 21% | Modest wage increases and business investments | Republicans support further cuts; Democrats propose higher rates | 40% drop in corporate tax revenue initially; recovery post-2020 |

| Immediate expensing of capital investments and research | Increased capital investments by approximately 11% | Bipartisan agreement on need for reform prior to implementation | Corporate profits surged beyond expectations during the pandemic |

| Child Tax Credit extension with scheduled expiration | Tax policies resulted in lower-than-expected wage increases | Tax debate re-emerging as provisions expire in 2025 | Analysis ongoing to understand tax revenue dynamics |

Summary

The 2017 Tax Cuts and Jobs Act was a significant reform, reshaping the corporate tax landscape in the U.S. This law has generated ongoing debate regarding its effectiveness and impact on the economy, specifically concerning the extent of wage increases and corporate tax revenues. As key provisions of the Act, including the reduced corporate tax rate and child tax credits approach expiration in 2025, the political discourse intensifies, with both parties presenting contrasting views on tax policy. Nevertheless, studies indicate a rise in capital investments due to the Act, suggesting a complex relationship between tax cuts and economic performance. Understanding the full ramifications of the 2017 Tax Cuts and Jobs Act will be crucial for lawmakers as they prepare for the upcoming tax legislative battle.